World Economic Data: Yen Past 150, Eurozone Negative GDP Print

World Economic Data: Yen Past 150, Eurozone Negative GDP Print

Trading Economics: Japanese Yen

Weakening Yen And its Battle With Sovereign Debt

Bank of Japan is stubborn on its interest rates (messaging: same policy) not to increase their 10-year Bond target above 1%. That positioning comes from its national debt standing at 217% of GDP, and higher interest rates would drive up its ever increasing borrowing costs. As Reuters reported earlier this year:

Reflecting snowballing debt, interest payments would nearly double from 8.6 trillion yen for fiscal 2023 to 17.1 trillion yen by the end of the forecast period [2033], the draft government estimate shows.

The government will present the estimate to parliament as a reference for lawmakers' debates on the next fiscal year's budget.

The Ministry of Finance, in separate projections issued earlier this month, said it could keep new bond issuance at some 32 trillion yen in the next few years.

Even assuming a rosy scenario in which the world's third-largest economy grows an annual 3% in nominal terms, the debt would continue to grow to just shy of 1,200 trillion yen at the end of the forecast period ending in March 2033, it showed.

[My emphasis. Japan’s economy will NOT grow at 3% in nominal terms without a small miracle. And even that won’t be enough…]

Data Source: World Bank (through 2021) Interest Payments on National Debt in Yen

Trading Economics: Japan’s Interest Rates

This as Japan’s economy declined from its peak in 2012; and then, stagnated since 2016 to 2021. 2022 it further declined as its currency weakened significantly as did all major currencies around the world versus the U.S. dollar.

Macrotrends : Japan’s GDP

Japan’s workforce is much older on average than other developed countries and their population is declining significantly along with their GDP.

Macrotrends: Japan’s Population

Japan is juggling on a tightrope its monetary policy to keep in check their National Debt from ballooning past 10 trillion (US) permanently. Going into COVID at $10.2 trillion US, Japan then added $1.5 trillion US in debt, then immediate paid that back down to $8.5 trillion. The US Fed raising rates while BOJ did not (as much - but actually did in proportionality to their economic size to the U.S.) drove their currency to destabilize. But a weak Yen makes their exports attractive to the United States (can buy more Japanese products with a dollar). Inflation is hitting locally as well - as it is around the world.

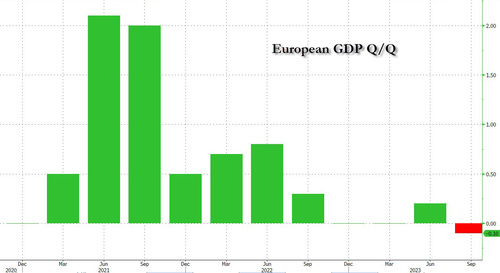

Eurozone GDP Down Below Zero

Quote:

The most obvious one being a further escalation of the war in the Middle-East, which could lead to seriously higher energy prices.

The economic impact of higher energy prices could be bigger than it was last time around. Governments no longer have the same fiscal firepower to cushion the blow, due to the increased cost of borrowing, whilst at the same time most consumers can’t rely anymore on a glut of pandemic savings. Indeed, in most countries, household savings adjusted for inflation are close to their pre-pandemic level.

Meanwhile, companies are also in a worse position to handle a new energy price shock. They already face (or are about to face) significantly higher financing costs and increasing labour costs, whilst the slowing economy likely means that they can’t fully charge those higher costs to their customers.

The economic price of a renewed energy shock could therefore be larger.

War is good for bankers, just not for anyone else that doesn’t want to eat the bugs.