Bank of America Reports Fiction

But don't let me tell you that...others will too!

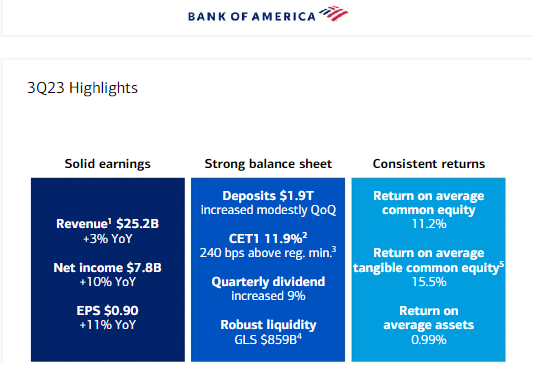

Above: BoA Scribd Report

One is not a banking expert. I have familiarity with income statements, balance sheets, cash flows, just like many of you likely do. I’ve not lived the day-to-day operations of a massive trillion-dollar operation such as Bank of America. However, macroeconomics trends, and other commentators that engage in data analysis from reports outside of a single firm, make it pretty easy to smell an overly rosy quarterly report from a top ESG-WEF connected Bank of [Soviet] America.

Charge offs are escalating among consumers going into the Holidays…

New credit card accounts and new originations (residential mortgages) are stagnating or going south. Same for vehicles and home equity.

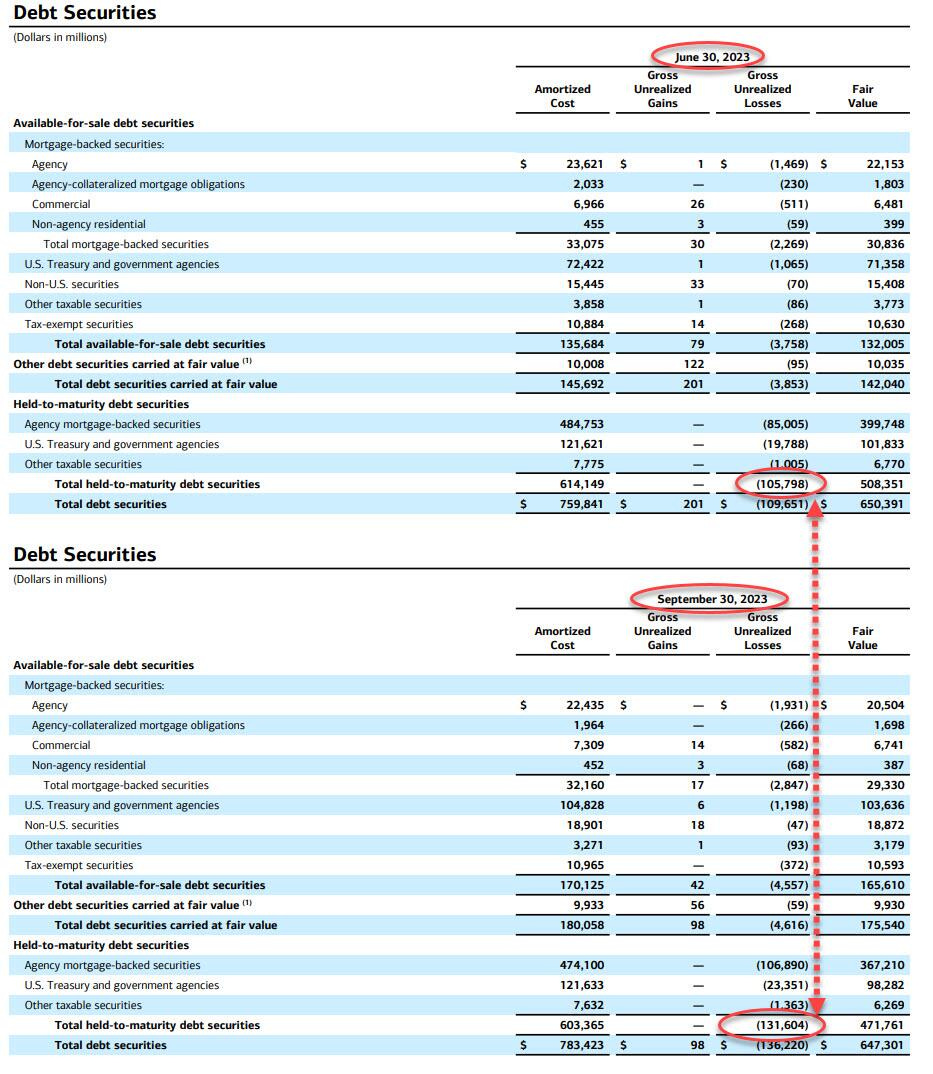

Held-to-maturity debt securities…growing by nearly $26 billion per quarter to $131.6 BILLION!

But even though others (more aware than I) had omened this problem, Bank of America pulled off their STOCK MARKET reporting miracle: Doug Casey’s take:

Those unrealized losses on investment securities grew (if we use BoA as an indicator of the banking network on the whole) - though it will get generally ignored on CNBC and the other Rah-Rah business networks.

Note: CNBC DID mentioned the HTM debt.

Casey’s blog noted that those unrealized losses topped a half-trillion and that gobbles up a lot of equity:

Through the end of Q2 2023, U.S. banks were sitting on $550 billion in unrealized losses from their holdings of long-duration Treasuries and MBSs. That’s nearly 25% of the total equity capital in the U.S. banking system.

Someone else who dug into the details, posited that:

Let's look at the 3Q "Summary Income Statement" shall we:

Total revenue net of interest expense is up less than 3% year over year

Why is revenue flat, if they're paying almost no interest on deposits and at the same time the rates on repo, commercial paper and money parked at the Fed are up over 5%?Provisions for credit losses are up over 30% year over year.

All the mortgage backed securities, which they've been buying hand over fist over the past decade and which pay a coupon of <4% are now underwater. Instead of marking these securities to market (or as available for sale), they are accounted for as being held to maturity, which means the bank has not yet recognized through income $131B of mark-down losses. What happens to the capital ratios of BofA if it had to take that $131B mark to market hit?Noninterest expense is up 3% year over year. So another strong year at BofA, but headcount costs are not matching the 5.1% rate of inflation. I'm sure Brian Moynihan would disagree about that.

Pretax pre-provision income is up only 1% year over year. What "best ever" earnings?

Income tax expense down 75% year over year. This large drop in tax expense is due to accounting gimmicks, not performance improvements of the core banking business.

So basically, BofA had a" record" earnings quarter due to accounting gimmicks, which had nothing to do with core lending and deposit-taking. If BofA recognizes the $131B of held to maturity losses, core capital ratios would take a 5% to 7% hit. What happens to a bank if its Tier 1 capital ratio drops to some level below the regulatory minimum? Where is the additional capital going to come from over the next 10 years, to offset $131B in credit losses? My guess, from underpaying employees and from shearing depositors.

At the point in this novel, called: “The Great Reset of the Monetary System so You’ll Eat Ze Bugs” I just look on with awe and financial contempt. It must be good to be so well-positioned to continue to lie and ignore reality. A Gangsta’s Paradise, if you will.

https://www.reuters.com/business/finance/bank-americas-unrealized-losses-securities-rose-1316-bln-2023-10-17/

Kane posts your pieces sometimes. That’s how I came upon your writing.